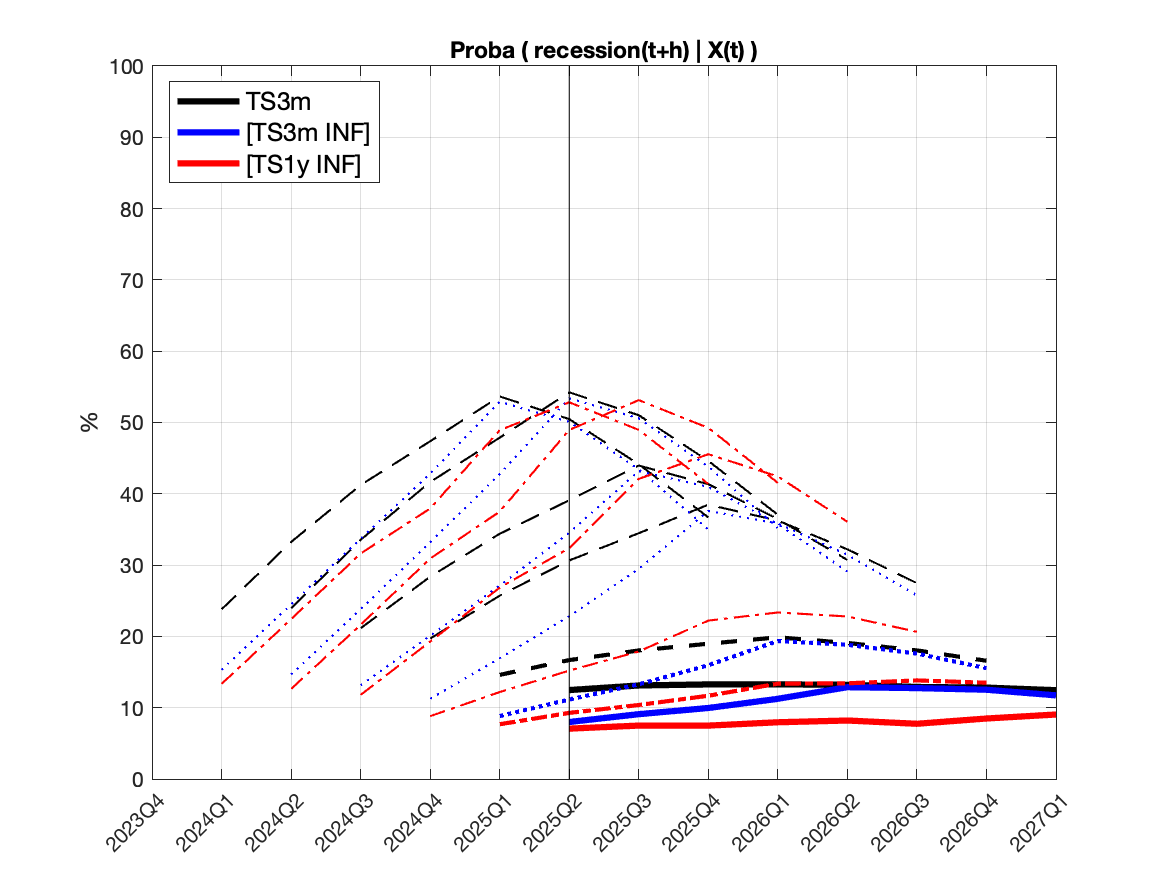

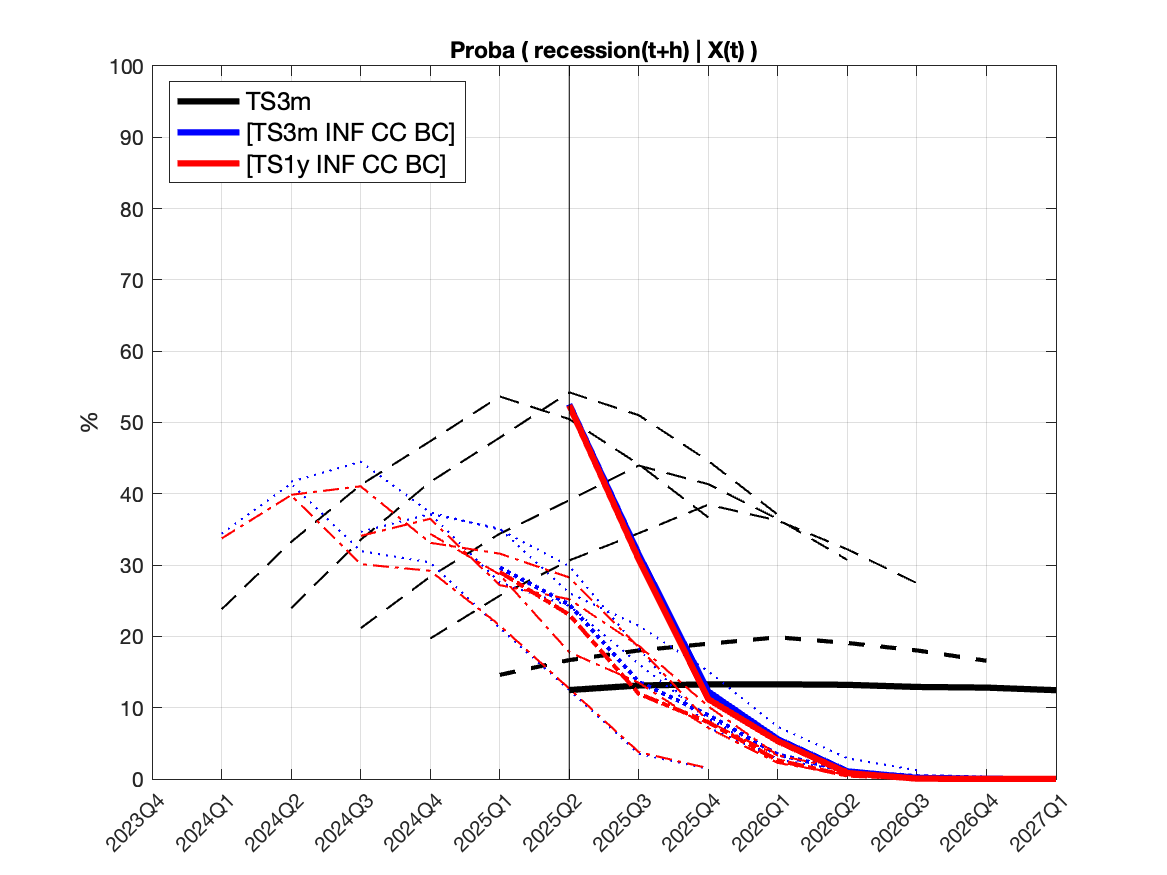

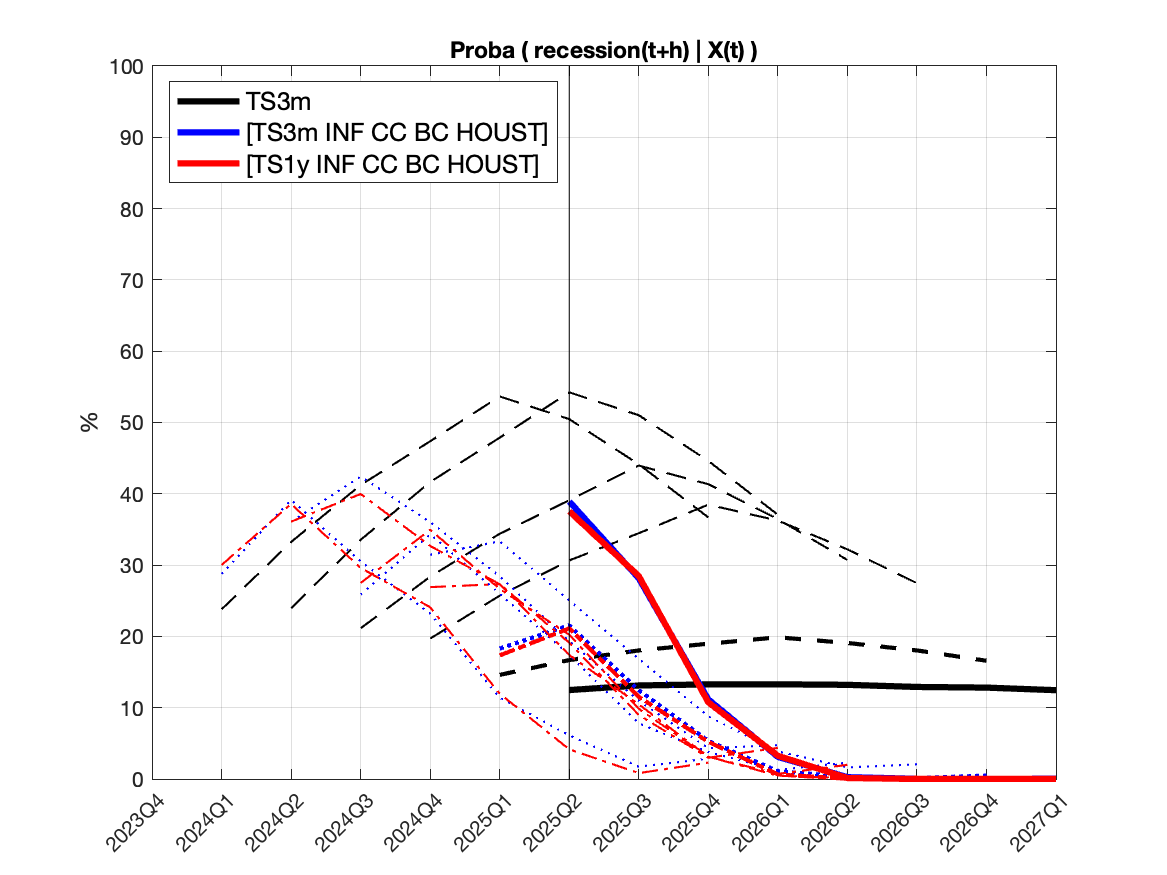

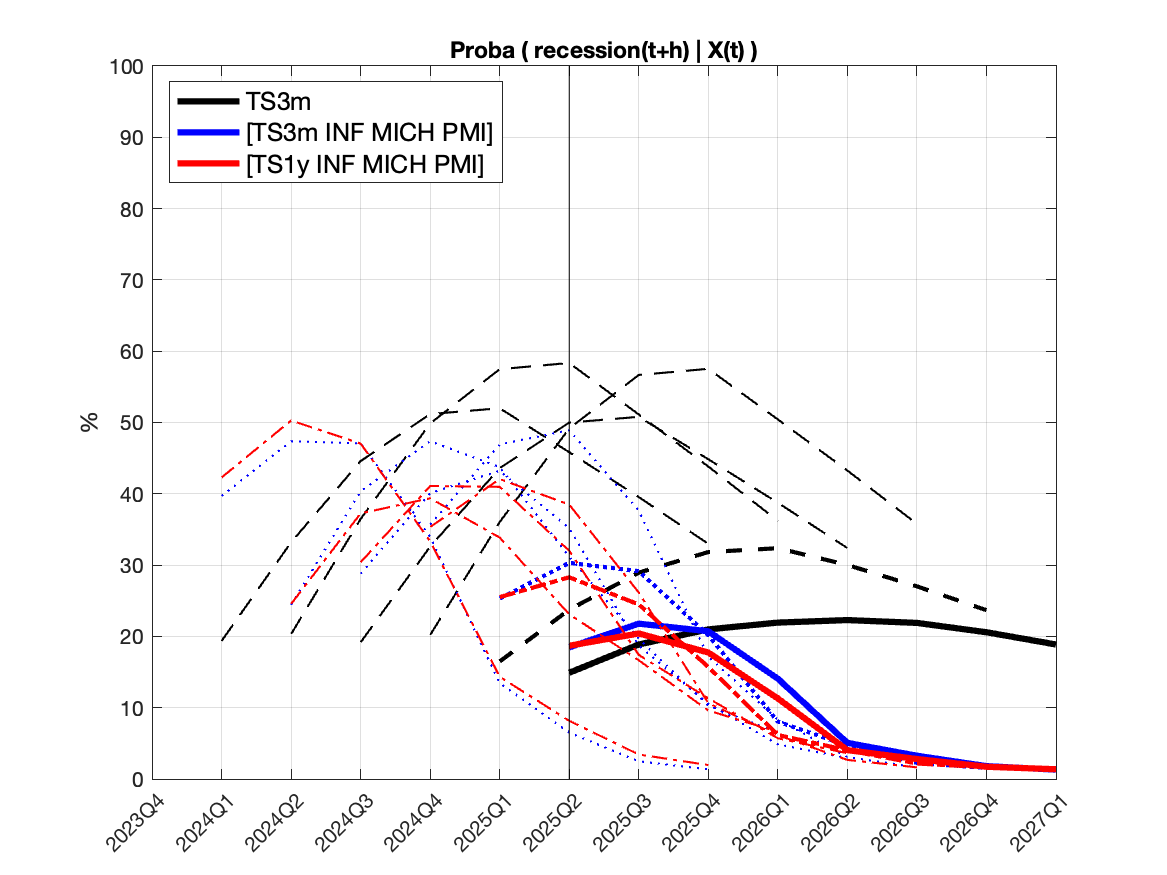

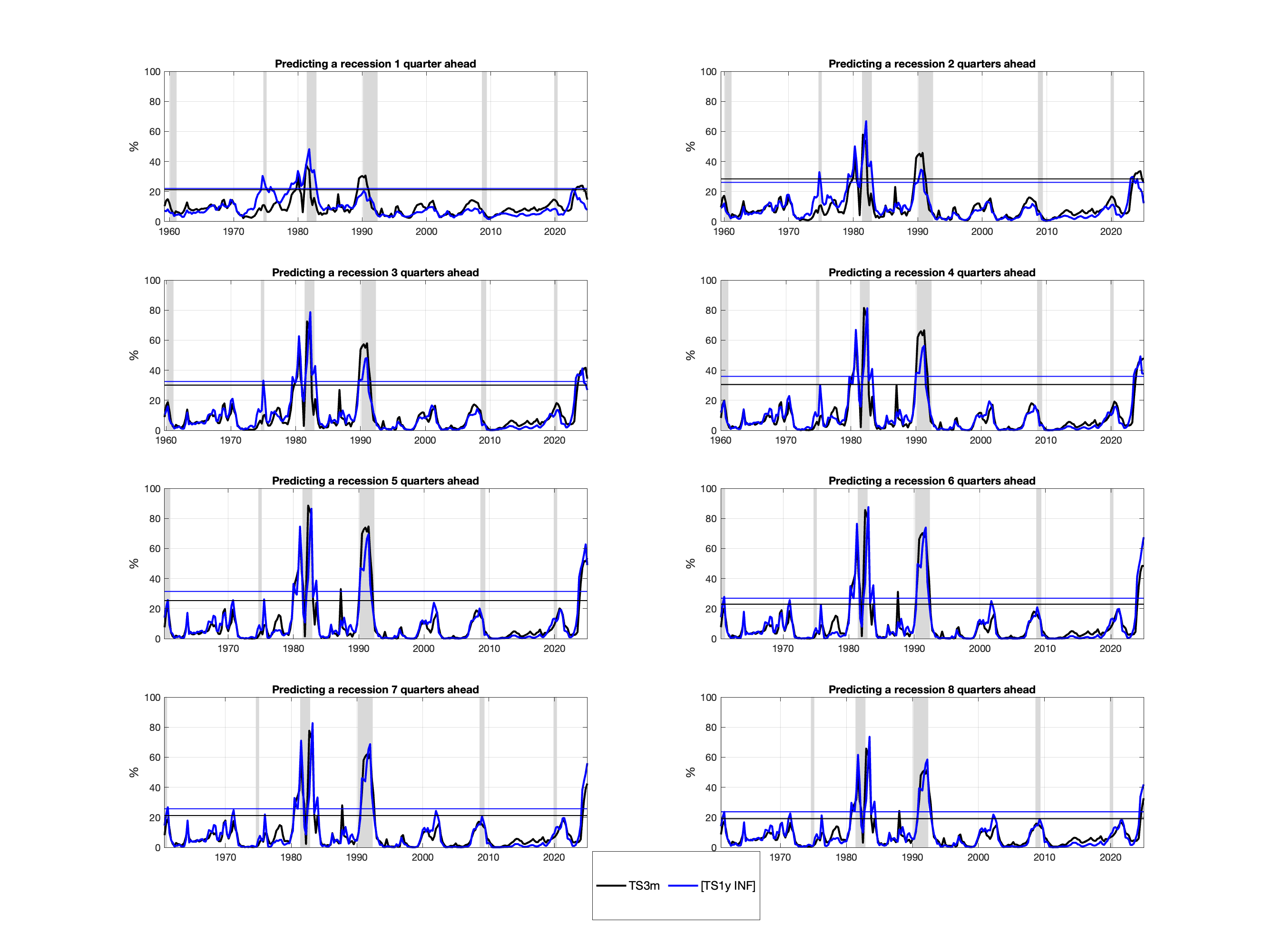

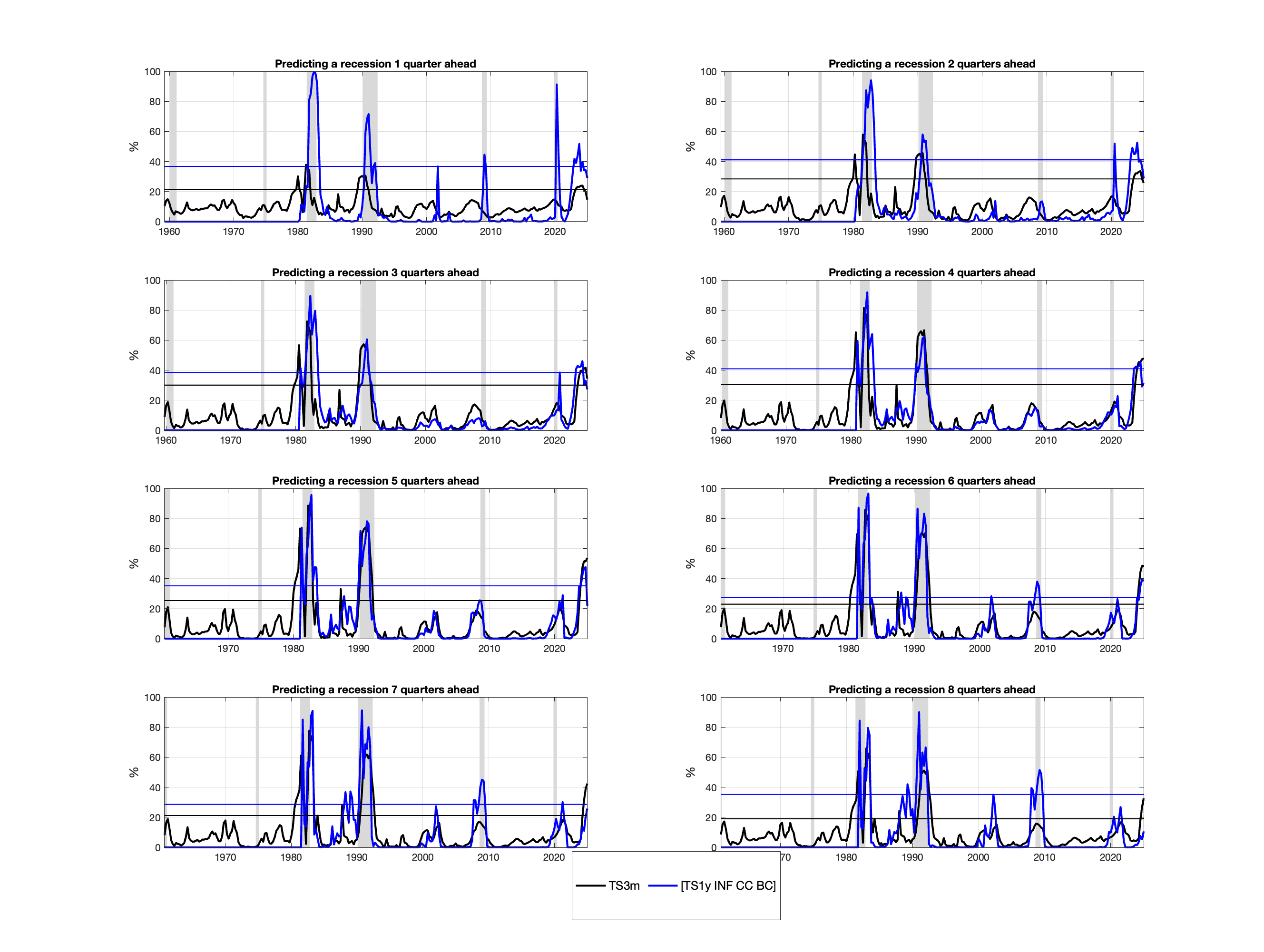

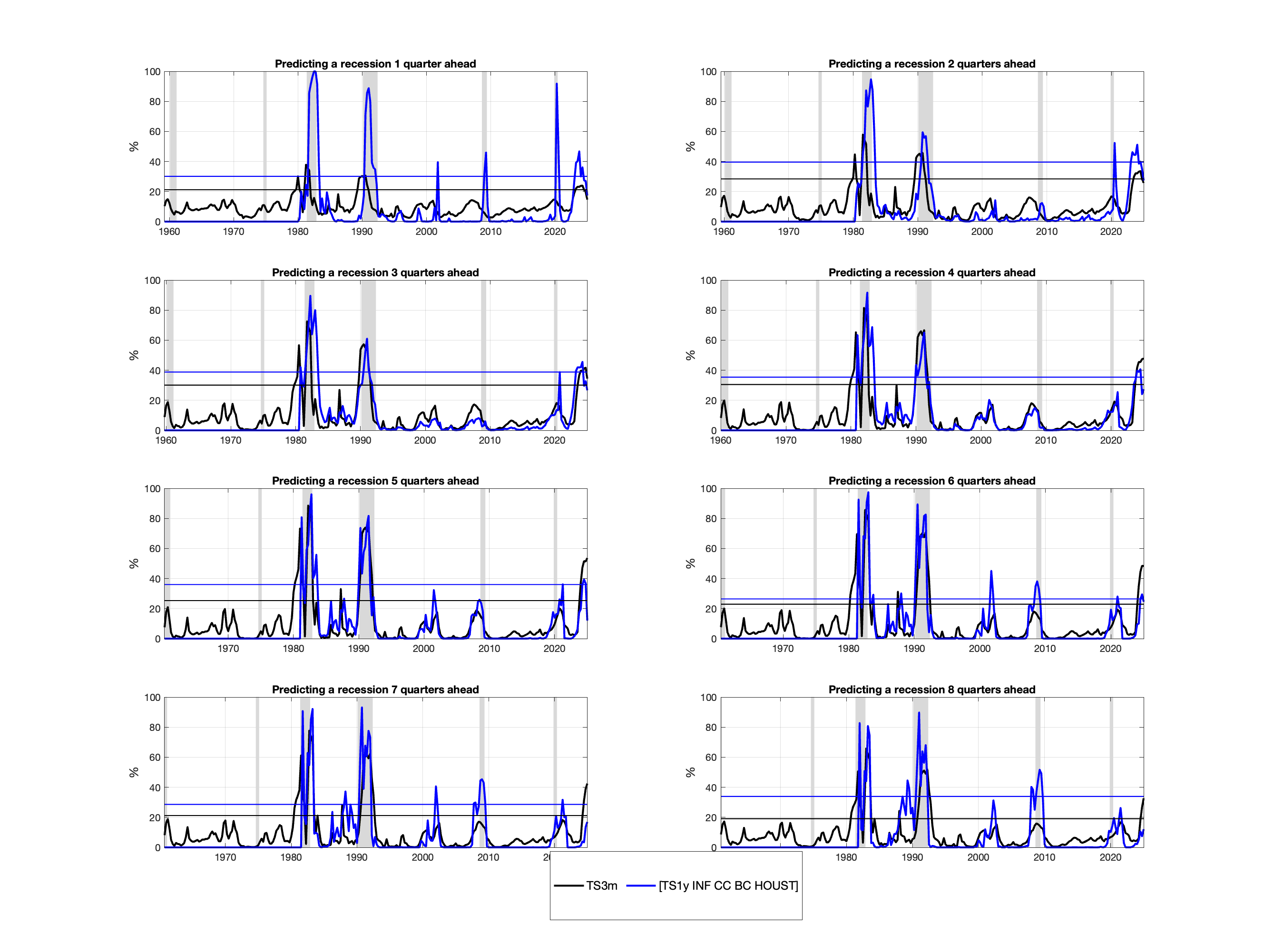

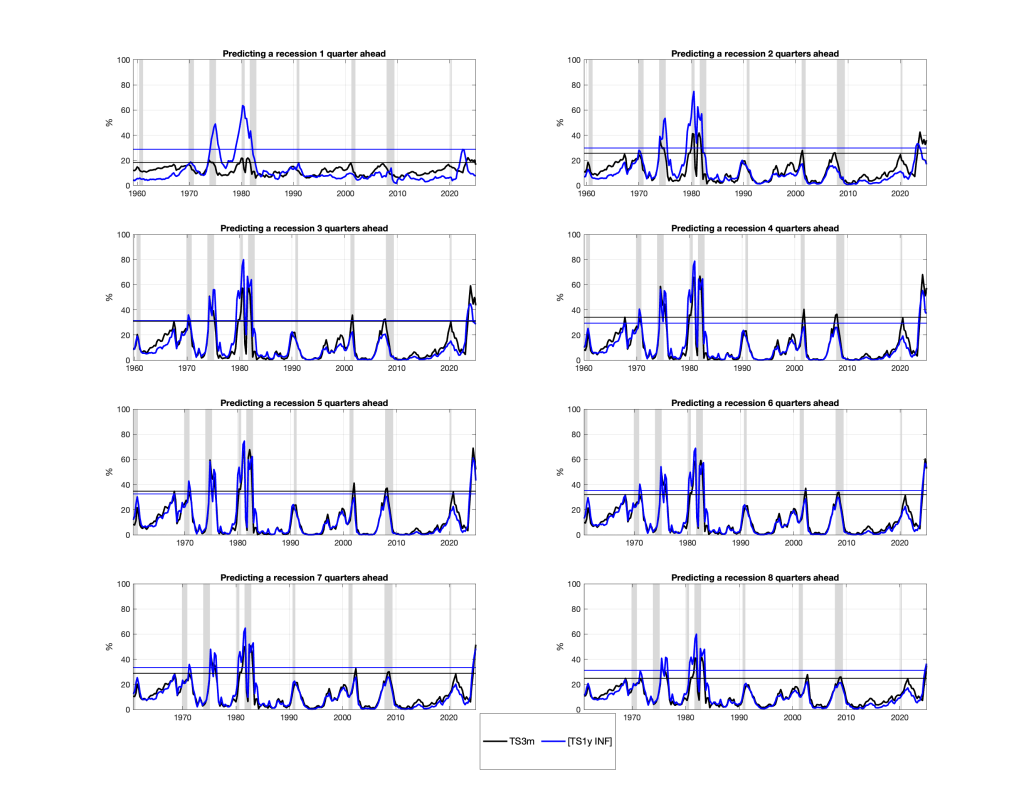

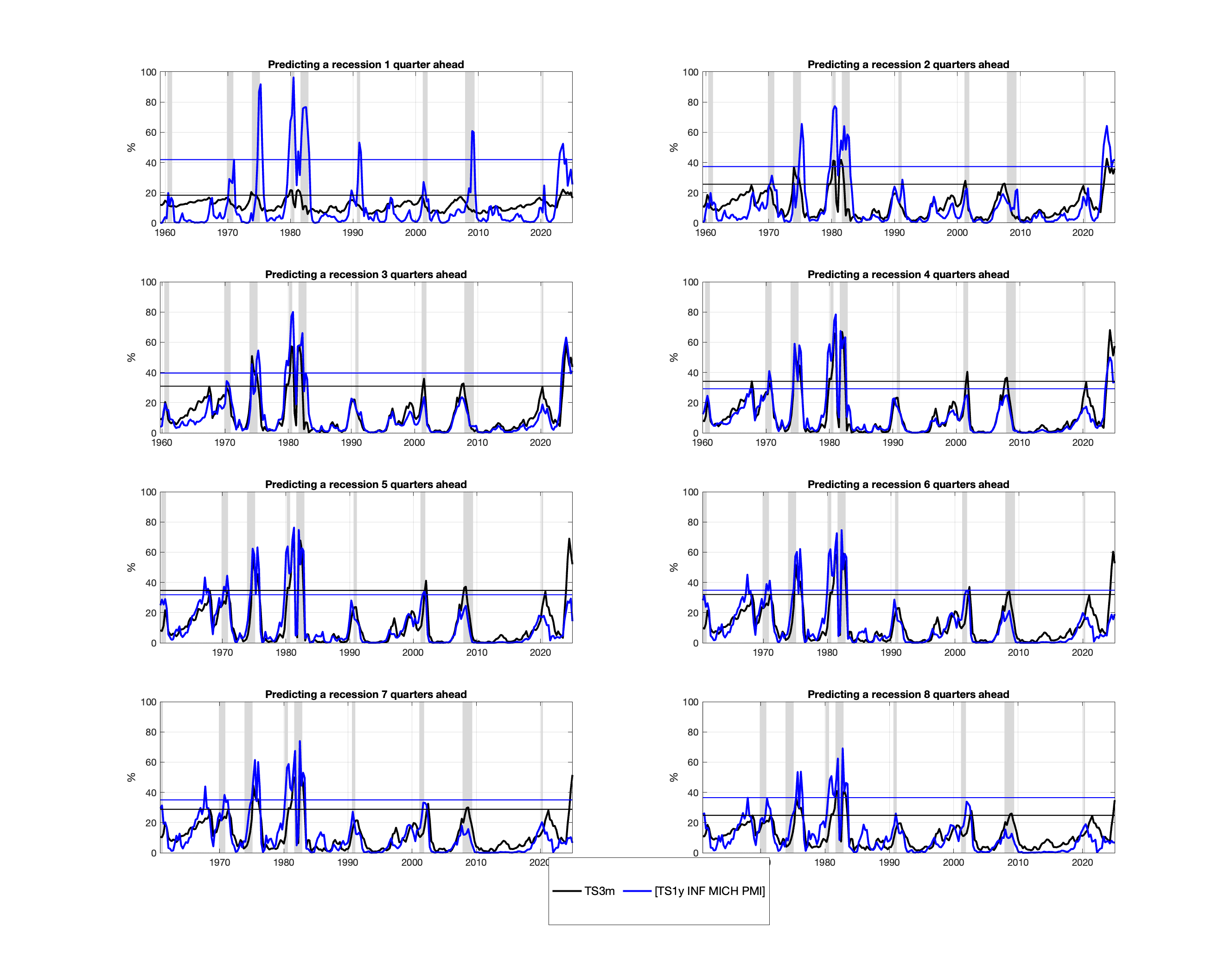

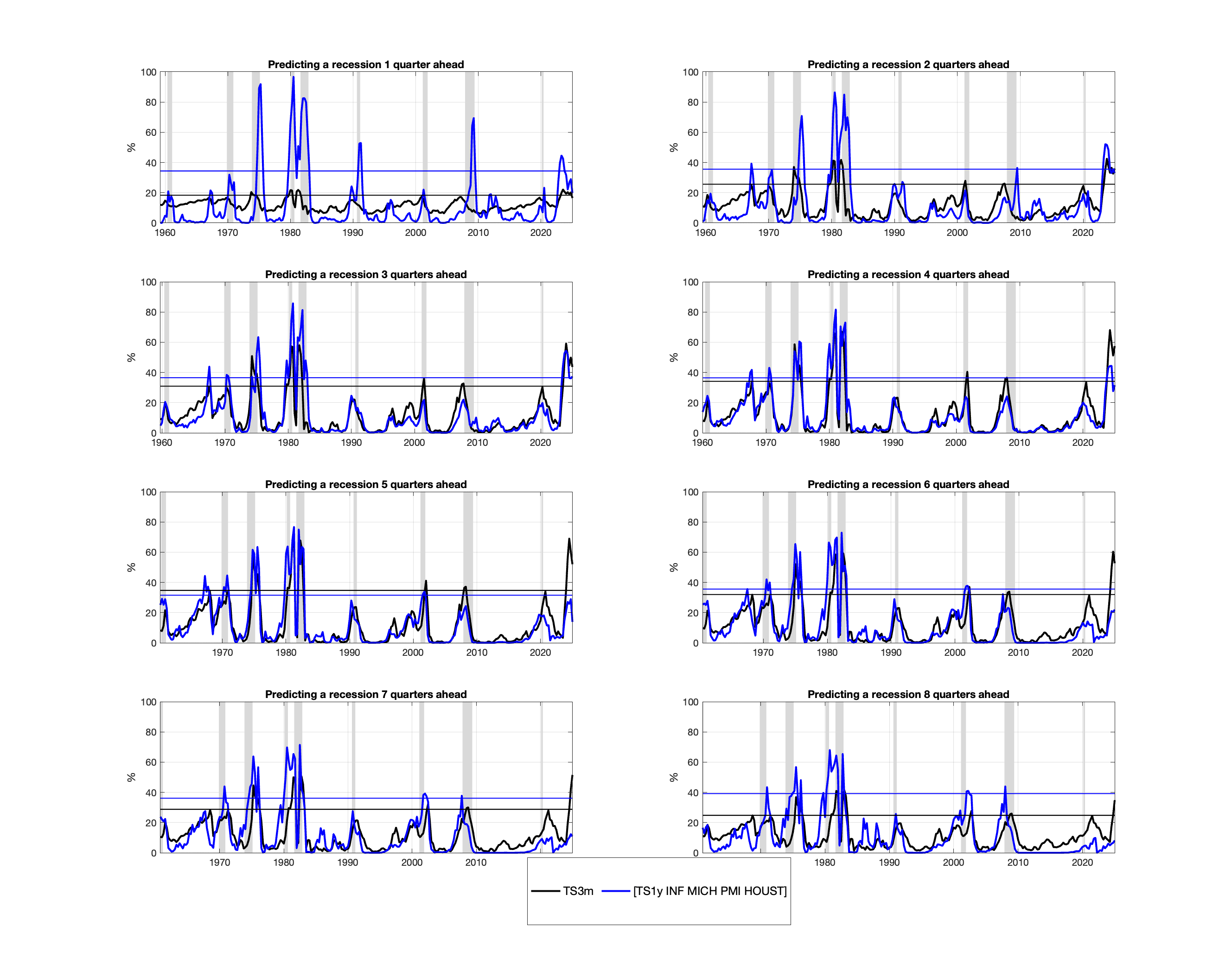

The figures below show forecasts of recession probabilities up to 8 quarters ahead. For example, the most recent forecast is based on information available as of March 2025, and probabilities are predicted from 2025Q2 through 2027Q1. We also show historical out-of-sample forecasts since 2022Q2. La version française de cette page est disponible ici.

Canada

United States

The methodology, based on Estrella and Mishkin (1998), employs a probit model with the following variables in the case of Canada: slope of the yield curve measured by the spread of 10-year and 3-month rates (TS3m) or 10-year and 1-year rates (TS1y); inflation measured by the year-on-year change in the CPI (INF); consumer confidence (CC) and business confidence (BC), and housing starts (HOUST). Both measures of confidence are from the Conference Board. In the case of the U.S., consumer confidence is measured by the University of Michigan survey (MICH) while business confidence is the purchasing managers’ index (PMI) from the Institute for Supply Management. Recession dates in Canada are from the C.D. Howe Institute and in the U.S. from the NBER Institute.

The models are estimated using quarterly data from 1959Q1 to 2024Q2, except for Canada, where CC and BC are included only from 1980 onwards due to data availability. The figures below illustrate the historical performance of the models.

Download the results : HERE

Historical performance

Canada

United States

References

Estrella, A. and Mishkin, F. (1998). Predicting US Recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80:45–61.